A Holiday Message from the Team at Offit Advisors

|

|

|

|

The team at Offit Advisors shares a message for you and your loved ones this holiday season.

|

|

|

|

Ben Offit interviewed Ned Atwater, Founder and Owner of Atwater’s during Leadership Baltimore County’s Economic Development day in early December.

|

|

What To Know Before Doing Any Year-End Portfolio Balancing

|

|

|

Check out this article from CNBC featuring Principal Ben Offit.

|

|

- Apple, Alphabet, Microsoft, Amazon, and Tesla, between them, have gained $6.5 trillion of value since their March 2020 lows. Apple alone has risen in value by an astonishing $1.85 trillion in just 433 trading sessions. Axios Markets, December 9, 2021

- On Monday of last week, 90% of the total bitcoin supply of 21 million has been mined. Yahoo! December 14, 2021

- The average NFL team sends more clothes to the laundry in one week than the average family does in two years. An average team can clean more than 5,500 pounds a week, compared to the average household which does 41.5 pounds. Consumer Reports, April 26, 2012

- “In trading, you have to be defensive and aggressive at the same time. If you are not aggressive, you are not going to make any money, and if you are not defensive, you are not going to keep it.” Ray Dalio

- The wait for micro-chips from order to delivery is now at a record 21.7 weeks. Bloomberg, October 6, 2021

- For years conventional wisdom held that millennials would become the generation that largely spurned homeownership. Instead, since 2019, when they surpassed the baby boomers to become the largest living adult generation in the U.S., they reached a milestone, accounting for more than half of all home-purchase loan applications. The Wall Street Journal, December 14, 2021

- Before the pandemic changed the working world, Americans ranked flexibility to set their own work schedules as the 74th most important out of 76 attributes associated with a successful and happy life. Now it sits at No. 2, second only to compensation. Axios November 16, 2021

|

|

A Holiday Note from Ben to Close Out 2021

Hello loyal readership,

I hope as you read this you are enjoying your favorite holiday beverage, kicking your feet up by the fire, and ready to enjoy this great article below. Today I’d like to discuss some lessons we have learned from 2021:

1. Inflation is not extinct - this has been the core economic issue of 2021 and most likely as well into 2022. This has been driven by supply chain issues and stimulus money flooding into the economy. With the supply chain issues, that may not go away for a while as many countries outside the US dont have Covid under control as much as the US and this can cause delays as our products are from global sources. Eventually inflation will come back to more normal levels as technology and innovation will drive inflation under control by creating various efficiencies.

2. Inflation has hurt your cash and bonds - if inflation has been a tad over 6% this year and your cash is earning near 0% and your bonds are earning less than 1-2%, then effectively you are losing money! Meanwhile, if stocks/equities have been up over 20% this year than you are making money. We have said it many times in this publication, that the best hedge against inflation is stocks/equities. The only reason to have bonds is to have them in a time of crisis or when the markets go down because when that happens, the bond portion of you portfolio usually goes up slightly, or maintains its value, or only goes down slightly And certainly less than equities.

3. Higher taxes haven’t happened…yet! - People were bracing themselves for higher taxes and it hasn’t happened yet. We were talking about getting rid of the step up in basis, capital gains being taxed at ordinary income tax rates, estate tax thresholds being way lower, and this hasn’t happened at all. Thank goodness for this because it would have caused some serious rushed planning towards the end of the year.

4. Speculative investments have become increasingly popular - Crypto, NFTs, SPACs, you name them. Many investors have grown increasingly attracted to these opportunities even though they have no real earnings, have no real underlying value, but people are buying into the notion of the future adaptation of these types of investments. I am not disputing the value of blockchain technology, cryptocurrency, or any of these innovations, but from an investing perspective it is impossible to know which of the 6,000 crypto current ices will be the winner and thus it is hard investment to make successfully. The challenge with this is that are ARE going to be people who make a fortune on these investments, but unfortunately it will only be around 1% of the lucky people and 99% of people are going to be investing in something that ends up being worthless. This is the essence of speculation. An analogy to this was in the early 2000’s there was a race to be the top internet search engine - and if you had invested in early leaders like Lykos, Ask Jeeves, etc you would have lost your money when Google finally arrived won. I believe this is a similar phenomenon going on with these types of assets

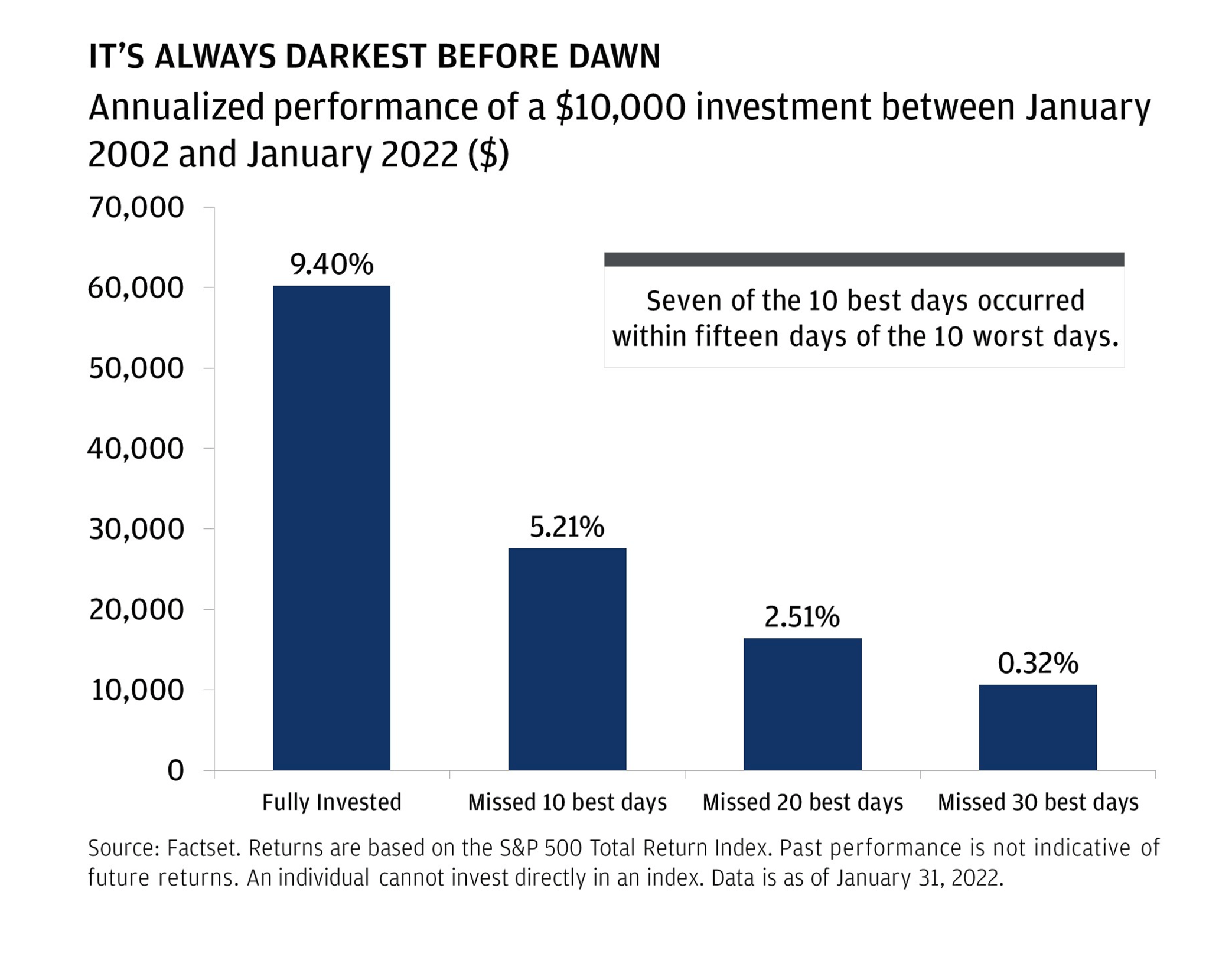

5. Market predictions for 2022? - Not so fast! As i have said many times i don’t pretend to know where the market will be and anyone who tells you that is not telling you the truth. It is ok to accept the fundamental truth that we never know where the market will be tomorrow, but we know that in the future it will be much higher than where it is today. In 2021, the market did terrific stemming from the stimulus money and people getting more and more vaccinated and going back to a more normalized life and business cycle. Also the rapid advancement and adaptation in technology has contributed to the market’s increase. So back to where the market will be in 2022? We don’t know but the market cares about where earnings of companies will be in 12 months from now for example. So if the market feels positive about the future then the market could continue to rise, if the sentiment is not positive it could go down. A lot of this will depend on what direction the various Covid variants may go.

Lastly, one final point for 2021. This is a time of year when people are thinking of tax strategies and being more gift and charitably oriented. 91% of charitable gifts are in cash even though most people don’t have 91% of their assets in cash. If you have stocks that grown and appreciated in value it would be a better strategy to gift that to a charity because you get the same income tax deduction but you ALSO get out of paying the capital gains tax on the sale of that stock and so does the charity. So be gift-smart and strategic everyone!

I hope you found this helpful and I will see you in 2022.

|

|

Stocks Decline in Late November as New COVID Variant Emerges

|

|

HIGHLIGHTS

- News of a new COVID variant, Omicron, sent markets to their worst daily drop of 2021 the day after Thanksgiving. Volatility, as measured by the VIX Index, rose by more than 10 points that same day, one of the largest daily advances for the VIX Index in its history.

- Equities took another leg down on the final trading day of November amid continued Omicron concerns. That decline was exacerbated by testimony from Fed Chair Powell who said the Fed would discuss ramping up their tapering at the December FOMC meeting.

- As would be expected during heightened equity market volatility, a flight to quality ensued into U.S. Treasuries late in the month. The 10-year U.S. Treasury yield closed 11/23 at 1.67%, but Treasuries rallied to end the month with the 10-year yield ending November at 1.43%.

- The U.S. economy picked up some momentum during the fourth quarter compared to the third quarter. However, continued high inflation readings and new concerns on the impact of Omicron overshadowed other economic data.

- Volatility returned with a vengeance in late November. Much is yet to be learned about Omicron and its potential impact, but as more details on this variant emerge, in the near term, markets will likely react accordingly – good or bad.

EQUITY MARKETS

The wind came out of the sails of equities late in the month as news of the new Omicron variant emerged. With this backdrop, large-cap growth outperformed other areas of the market for the month. The Dow Jones Industrial Average, the S&P 500 and the NASDAQ Composite put in new all-time highs during November, but only the NASDAQ was able to hold onto gains for the month. The year-to-date numbers now show a clear advantage for growth stocks in the large-cap space, but value still rules in the mid and small-cap universe.

The CBOE Volatility Index, or VIX Index, spiked higher late in the month as the Omicron news hit the market. The VIX Index ended October at 16.26, but rose to 27.19 by the end of November. Our expectation of a more volatile second half of 2021 has materialized. Not only is the emerging news on the Omicron variant increasing volatility, but uncertainty surrounding the future course of the Fed’s actions and whether it might speed up the tapering in the months ahead (meaning a more hawkish Fed) has also unsettled the markets.

Size and style mattered once again in November. We still believe that the value/growth disparity that reached a peak last year will likely continue to shift as we move into 2022 with value improving on a relative basis. We continue to use our disciplined approach of seeking out what we believe are high-quality companies with improving business conditions at good prices. These types of companies can be found in both the value and growth universe, but with value stocks improving over the last year or so, that has benefitted our approach.

The numbers for November were as follows: The S&P 500 declined -0.69%, the Dow Jones Industrial Average fell -3.50%, the Russell 3000 dropped by -1.52%, the NASDAQ Composite eked out a 0.33% gain, and the Russell 2000 Index, a measure of small-cap stocks, was hardest hit, down -4.17%. Through eleven months of 2021, returns in the same order were as follows: 23.18%, 14.61%, 20.90%, 21.28%, and 12.31%, respectively.

We will continue to monitor how trends shift in the coming months and whether the recent gains in large-cap growth stocks develop more footing or whether small and mid-cap stocks, along with value, return to their leadership roles that started late last summer. Large-cap growth stocks have been the clear leader over the last couple of months.

Looking closer at style, the headline Russell 1000 Index declined -1.34% for the month with a year-to-date gain of 21.53%. The Russell 1000 Growth Index showed some of the best gains in November by increasing 0.61% and this index is up 24.95% year to date. The Russell 1000 Value Index relinquished its leadership role recently and that trend continued in November. For the month, it declined -3.52%, which put the year-to-date gain at 17.73%. For small-caps, value continued to outperform growth on a relative basis. The value/growth disparity is much more pronounced in small-caps for the year to date with the Russell 2000 Value Index up 23.24%, while the Russell 2000 Growth Index has gained a mere 2.38% during the same timeframe.

International markets once again lagged U.S. stocks in November. The MSCI Emerging Markets Index declined -4.08% in November, which keeps this index in negative territory (down -4.34%) for the year to date. The MSCI ACWI ex USA Index, a broad measure of international equities, fell -4.50% in November, which lowered the year-to-date gain to only 3.54%. Following the trend of recent years, U.S. stocks have continued to outperform their international counterparts. Within international markets, developed countries have done better than emerging markets so far in 2021.

FIXED INCOME

After surging higher during the first quarter of 2021, the yield on the 10-year U.S. Treasury dropped over the next four months. That streak ended in August as yields moved higher and that move higher continued in September and October. Although that trend was continuing for most of November, the late month news on the new Omicron variant spurred a flight to quality and as a result, yields dropped sharply. Overall, the 10-year U.S. Treasury yield closed October at 1.55% and it ended November at 1.43%. Bond sector results were mixed for the month with this backdrop.

Fixed income returns were as follows for November: the Bloomberg Barclays U.S. Aggregate Bond Index gained 0.30%, the Bloomberg Barclays U.S. Credit Index rose a modest 0.08%, the Bloomberg Barclays U.S. Corporate High Yield Index was off by -0.97% and the Bloomberg Barclays Municipal Index gained 0.85%. For the year to date, those index returns in the same order were as follows: -1.29%, -1.00%, 3.34%, and 1.35%, respectively. With only one month to go in the year, the Agg is close to posting only its fourth annual drop since its inception in 1976. This has been clearly a challenging year for bonds and, in particular, for U.S. Treasuries. High yield bonds remained the clear leader year to date and municipals have also enjoyed gains as concerns about higher taxes mount.

The 30-year U.S. Treasury Index gained 3.36% for the month, as the 30-year yield dropped, but it is still off by -2.61% year to date. The general U.S. Treasury Index gained 0.77% in November and is down -1.82% year to date. We continue to maintain our long-standing position favoring credit versus pure rate exposure in this interest rate environment.

Source: Clark Capital Benchmark Review, November 2021

|

|

S&P 500 Index is an unmanaged group of securities considered to be representative of the stock market in general. You cannot directly invest in the index.

Dow Jones Industrial Average - The Dow Jones Industrial Average is a popular indicator of the stock market based on the average closing prices of 30 active U.S. stocks representative of the overall economy.

NASDAQ Composite Index measures all NASDAQ domestic and international based common type stocks listed on The NASDAQ Stock Market. Today the NASDAQ Composite includes approximately 5,000 stocks, more than most other stock market indices. Because it is so broad-based, the Composite is one of the most widely followed and quoted major market indices.

Russell 2000® Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 8% of the total market capitalization of the Russell 3000 Index which includes the 3,000 largest companies in the U.S., based on market capitalization. As of the latest reconstitution, the average market capitalization was approximately $762.8 million; the median market capitalization was approximately $613.5 million. The largest company in the index had an approximate market capitalization of $2.0 billion and a smallest of 218.4 million.

Russell 1000® Growth Index measures the performance of those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values.

Russell 1000® Value Index measures the performance of those Russell 1000 companies with lower price-to-book ratios and lower forecasted growth values.

Government bonds are guaranteed by the U. S. Government and, if held to maturity, offer a fixed rate of return and fixed principal value.

|

|

|

Securities offered through Kestra Investment Services, LLC (Kestra IS), Member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS), an affiliate of Kestra IS. Offit Advisors is not affiliated with Kestra IS or Kestra AS. Offit Advisory Services, LLC is a tax firm but neither Kestra IS nor Kestra AS provide legal or tax advice and are not Certified Public Accounting firms.For more information on the Five Star Wealth Manager and the research/selection methodology go to: www.fivestarprofessional.com. Investor Disclosures: https://bit.ly/KF-Disclosures

|

|

|

|

|

|